Leveraging the power of alternatives across all ages

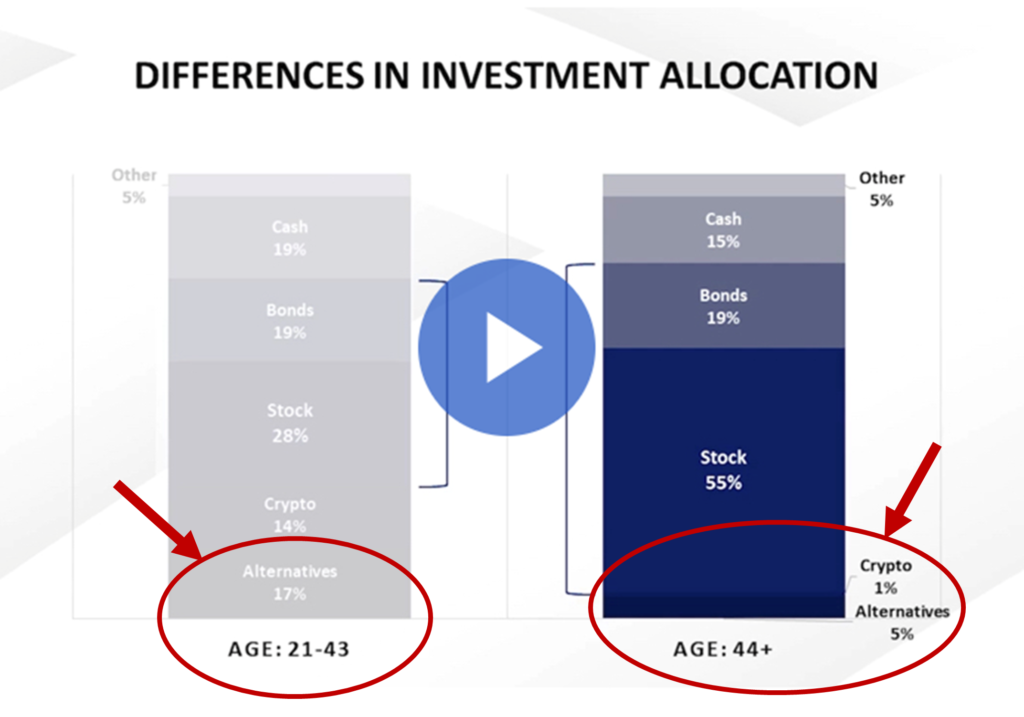

Perusing the financial news this week, the report on Bank of America’s latest survey caught my eye. Every year, Bank of America conducts its Private Bank Study of Wealthy Americans to assess investment trends and attitudes among wealthy individuals. This year, the survey revealed a significant generational gap between how younger investors are choosing to allocate their investments compared to their parents’ generation (and, I suspect, their parents themselves). Here’s the chart that caught my eye—and my circles indicate why:

(Image Copyright: Bank of America)

As someone who focuses a good portion of my time looking at the opportunities provided by alternative investments within our own portfolios, the fact that younger investors are increasingly turning to alternatives—and that older generations are not—was not so much a surprise at it was a confirmation that the choice to apply alternatives to help our clients of every age reach their investment goals is a good one.

While there are many reasons why I feel that statement is true, here are a few at the top of the list:

- Alternatives ‘play well’ with stocks and bonds. In general, stocks and bonds have a push-pull relationship in an investment portfolio. When stocks are stronger, bonds are typically weaker. The same is true in reverse, which is precisely why a diversified portfolio includes both asset classes. By bundling assets that aren’t highly correlated to the same market or economic conditions, a diversified portfolio is more likely to deliver positive returns over the long term. However, this push-pull dynamic doesn’t always hold true. There are times when stocks and bonds both lose value at the same time, washing away the diversification power of the ‘normal’ stock-bond relationship.

- Alternatives add diversity to help reduce overall portfolio risk. When this happens, alternatives (which also tend to deliver positive returns when equities are up) can help smooth the ride for investors by adding an extra layer of diversification that helps further reduce risk exposure. By providing access to categories of assets that are not contained in the traditional investment buckets of stocks, bonds, or cash—and that have the potential to move in opposite trajectories compared to these traditional investments—alternatives are one of the best diversification tools available to investors today.

- Our approach is flexible and fluid. Our approach to alternatives gives us the freedom to use different strategies at different times. Current economic trends may influence our preferred exposure to a certain asset class. For instance, if interest rates are poised to sharply increase, we may bump up our use (or exposure) of ‘Unconstrained Bond Funds’ or ‘Managed Futures’. And in times of geopolitical turmoil, we may rely more heavily on what’s called our ‘Global Macro’ strategy that uses changes in the valuation or devaluation of certain global currencies to our advantage.

- Our LCM Alternatives Collection creates flexibility to support our clients’ unique goals. The reason the findings of the Bank of America study bother me is because I feel strongly that many investors in the 44+ age group would be wise to increase the use of alternatives in their portfolios. That said, one size rarely (if ever!) fits all, which is why we offer two strategies to meet the diverse needs of our clients: a Growth Strategy & an Income Strategy. In general, our clients typically fall into two groups: those focused on asset growth and those focused mainly on capital preservation & income. Interestingly, your age, level of assets, or whether you are actively earning an income doesn’t automatically place you into one group or the other. Many of our older, retired clients view capital preservation as their primary objective. The same is true, however, for many of our ultra-high-net-worth clients who have no need to grow their assets. And while many younger, high-earning professionals are striving to grow their portfolios aggressively, we also have older clients who, having accumulated a high level of wealth, are willing to take on greater risk in order to leave behind a more substantial legacy to future generations. We know that the most appropriate investment strategy is dictated by your specific short- and long-term investment goals. By taking the time to understand those goals, we can determine if an alternatives strategy is a good fit for your portfolio and, if so, which strategy is right for you.

Studies like the Bank of America survey are powerful tools for identifying trends across a large population. That said, I can rest easier at night knowing that, unlike “most wealthy Americans over 44” who are investing in alternatives either very little or not at all, our clients of every age have the option to take advantage of the investment power of alternatives to help reach their investment goals.

To learn more about alternative investments, including what they are, how we use them, and how they can add value to your portfolio (at any age!), download: The LCM Guide to Alternative Investments. And if you have any questions at all, please reach out. We are always at your service!

← Back to Insights

Principal & Senior Investment Officer