The ‘Santa Claus Rally’ is something investors have learned to hope for every year. As illogical as it sounds, this rally appears in the weeks leading up to December 25, and it often brings a nice bump in gains for the end-of-year stock market numbers. Unfortunately, it doesn’t look like investors will be receiving any gift of the kind this year. The reason: Wall Street is holding on to concerns over inflation, Fed policy, and recession risk.

I’m still surprised at last week’s downturn, especially considering the recent news that could have easily pushed the market in the opposite direction. First came a rather benign report on the Consumer Price Index (CPI), including data that seemed to indicate a slowing of inflation—and that actually came in under estimates that already incorporated some slowing of inflation. That, in turn, gave the Fed the wiggle room needed to opt for a smaller rate increase compared to their recent rate decisions. The Fed did just that last Wednesday, raising its target federal funds rate by just half a percent—a small reprieve from the incredible pace of rate hikes throughout the year. So why the turbulence? Why isn’t Santa Claus rallying this year? Here are three factors that are (probably) creating such bad weather for the market today:

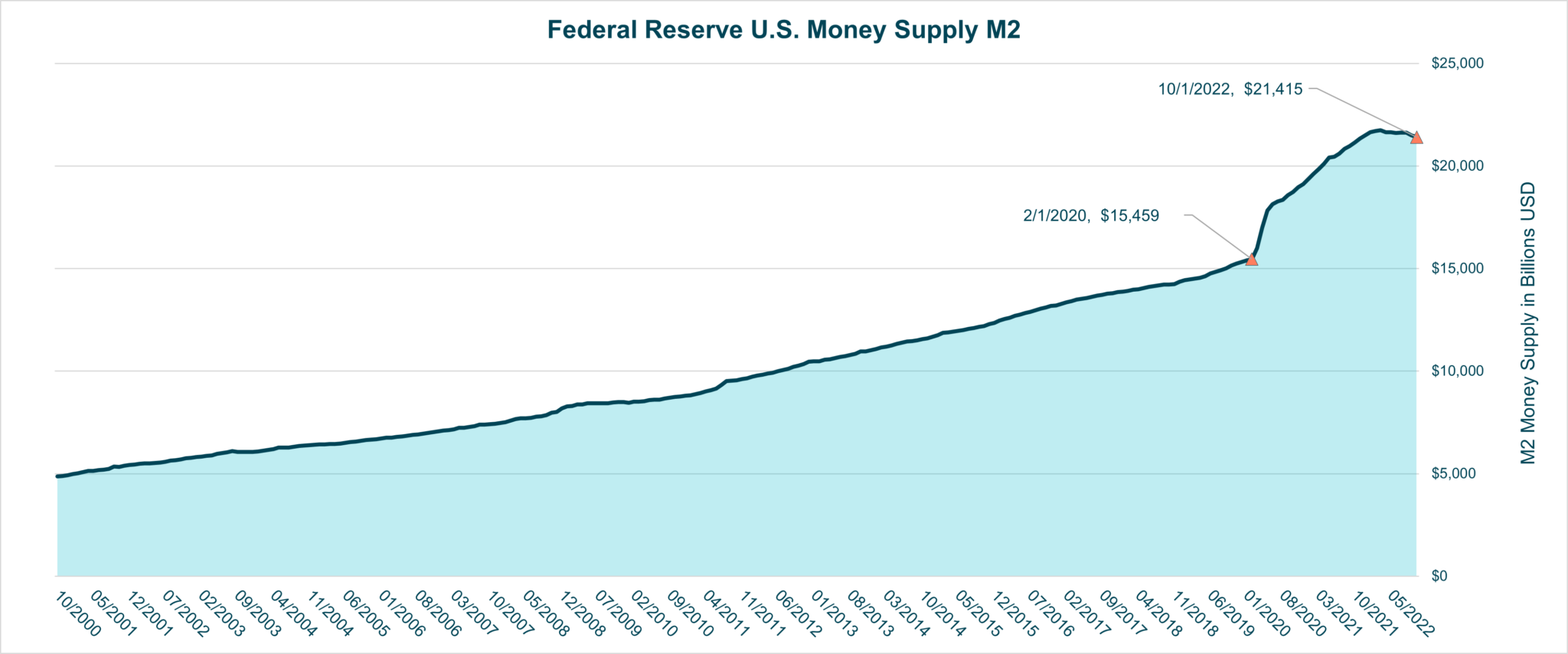

Source: Bloomberg

In short, it worked. Perhaps a bit too well. When elevated levels of inflation first appeared, the Fed reacted by justifying the rise as covid-related. From the Fed’s perspective, the ‘blip’ was transitory. Once the Fed finally understood and acknowledged that inflation had officially arrived and was likely to remain, monetary policy was quickly changed to focus almost solely on reining in inflation through increased interest rates.

When will this revised monetary policy start making a difference? History tells us that it takes about a year of restrictive monetary policy before inflation begins to respond to the actions of the Fed. The first, tepid rate hike of 0.25% was put in place in March 2022. Since then, the Fed increased rates 0.50% in May, followed by four hikes of 0.75% each. In short, this has been the fastest pace of rate hikes in history! Will that fact bring change faster? Will we need to wait another 3-4 months to see an impact on inflation? Hopefully, the Fed’s aggressive action will help the economy and the markets change course sooner rather than later.

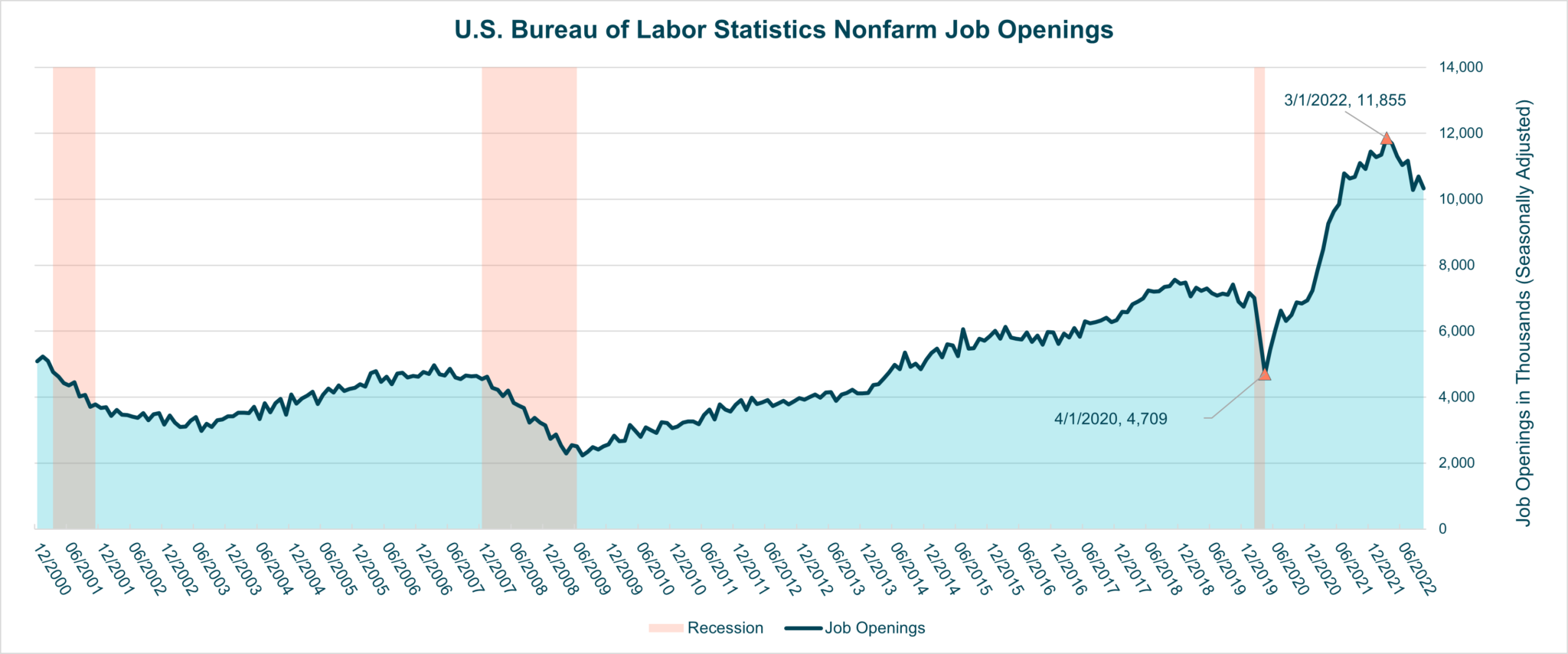

Source: US Bureau of Labor Statistics

Interestingly, even in the face of hawkish monetary policy, the unemployment rate itself has held steady. This is most likely explained by the still-elevated number of job openings; even when workers are laid off, there are many options for re-employment. Will that keep the National Bureau of Economic Research, the body responsible for the official declaration of recession, from announcing that recession has arrived? It’s doubtful. The weightier indictor of a recession is a broad slowing of economic activity, sometimes summarized as two consecutive quarters of negative GDP growth. But whether a recession becomes official or not, tougher economic times are likely headed our way. The question the markets are digesting now is just how tough—and how long—that era will be.

All that said, the sharp fluctuations in market sentiment are likely to continue. Market participants (read investors, but primarily institutional investors that tend to be the key drivers of financial market trends) are bifurcated, with some calling for a long and deep recession, and others projecting a short and shallow recession. Until the economy delivers some clarity, it’s going to be a bumpy ride. Still, there are plenty of reasons for optimism:

As we near the end of 2022, we see good things ahead. Yes, it may take some time for the current situation to play out in full (so don’t expect a Santa Claus rally to ‘save’ annual returns this year!), but as every investor knows, even down markets offer opportunity—and those who have the fortitude to ride out the storm usually come out ahead in the end. Hang in there, and if you have any questions, don’t hesitate to reach out. Our team will be taking time to enjoy family and friends during the holidays, but we are never more than a phone call away.

Have a wonderful holiday and a happy, prosperous New Year!